Hormuz Reopening: Will It Halt the Surge Towards $190 Oil?

The global energy market has endured unprecedented turmoil since late February 2026, when the ongoing Iran war effectively blockaded the Strait of Hormuz. Brent crude prices surged by 65% by the end of March, climbing above $120 per barrel, with some projections indicating a potential rise to $190 under prolonged disruption scenarios. Liquefied natural gas (LNG) prices also spiked, with Asian benchmarks increasing by nearly 40%, creating severe supply shortages. Amid this crisis, expectations are mounting for a US-Iran peace agreement to unblock the Strait of Hormuz, potentially normalizing international oil and natural gas markets.

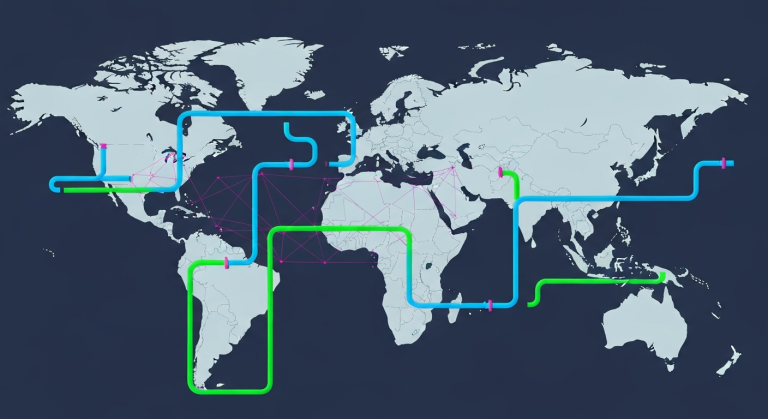

The Strait of Hormuz is a critical energy chokepoint, through which approximately 20-25% of global seaborne oil trade and about 20% of global LNG trade typically passes. A significant majority of LNG exports from Qatar and the UAE, specifically 83%, transit this strait, primarily destined for Asian markets like China, India, and South Korea. The blockade caused a staggering 10.1 million barrels per day (mb/d) crash in global oil supply in March 2026, with Persian Gulf producers experiencing a 14.4 mb/d reduction from pre-war levels. Consequently, global oil inventories have plummeted to their lowest levels since 2003.

Strategic Insight: Iran’s Leverage and Shifting Market Dynamics

Iran has long leveraged the Strait of Hormuz’s strategic geographical position as a key point of influence. Threats of closure have historically exerted significant pressure on the international community, directly impacting global energy security. A peace agreement leading to the unblocking of the Strait carries strategic implications far beyond mere logistical restoration. It would allow Persian Gulf nations to normalize oil and gas production, alleviating significant global supply imbalances, particularly for Asian markets that were most vulnerable to the disruption.

From a market perspective, reopening the Strait would stabilize energy supply chains, pushing oil and gas prices downwards. The reduction in elevated shipping costs and insurance premiums, coupled with the dissipation of the uncertainty premium, would lower overall energy expenses. Asian economies, having been disproportionately affected by the Hormuz blockade, stand to gain significantly from renewed supply flows.

Competitive Landscape: OPEC+ Strategy and Non-Middle East Suppliers

During the blockade, Persian Gulf nations were forced to drastically cut crude oil production. Key producers like Saudi Arabia, Iraq, the UAE, and Kuwait collectively suffered a loss of 9.28 mb/d in production between February and April 2026. An unblocked Strait would enable these countries to ramp up output, introducing a new dynamic into OPEC+ production strategies. Furthermore, the potential resumption of full Iranian oil exports could add significant supply to the global market.

Conversely, non-Middle Eastern LNG exporters, such as the United States, increased their supply to Europe during the blockade, partially filling the void. With the Strait of Hormuz normalizing, the competitiveness of Middle Eastern LNG would be restored, intensifying the global LNG market landscape. This shift presents both opportunities and challenges for nations that have pursued energy diversification and supply source strategies over the long term.

Actionable Conclusion: Pace of Recovery and Continued Vigilance

The reopening of the Strait of Hormuz would send a powerful positive signal to global energy markets. However, a complete return to normalcy will likely be gradual. Repairing war-damaged infrastructure, restarting production, and replenishing historically low inventories will take considerable time. The EIA projects that even with a gradual resumption of traffic in Q3 2026, pre-conflict trade patterns may not fully return until early 2027.

Investors should closely monitor the specifics of any peace agreement, the pace of production recovery from Persian Gulf producers, and changes in global inventory levels. While short-term downward pressure on oil prices from increased supply and reduced shipping costs is likely, a geopolitical risk premium may persist in the long run. Energy companies must continue to prioritize supply chain resilience and invest in diversifying transport routes and energy sources. The energy security vulnerabilities of Asian markets also remain a critical factor requiring ongoing attention.

References & Sources